Biden v. Nebraska

Case Overview

CITATION

ARGUED ON

DECIDED ON

DECIDED BY

600 U.S. 477

Feb. 28, 2023

Jun. 30, 2023

Legal Issues

Does the HEROES Act grant the Secretary of Education the authority to cancel $430 billion dollars in student loans?

Holding

No, the HEROES Act only allows the Secretary to “waive or modify” existing statutory or regulatory provisions applicable to financial assistance programs under the Education Act, not to rewrite that statute from the ground up.

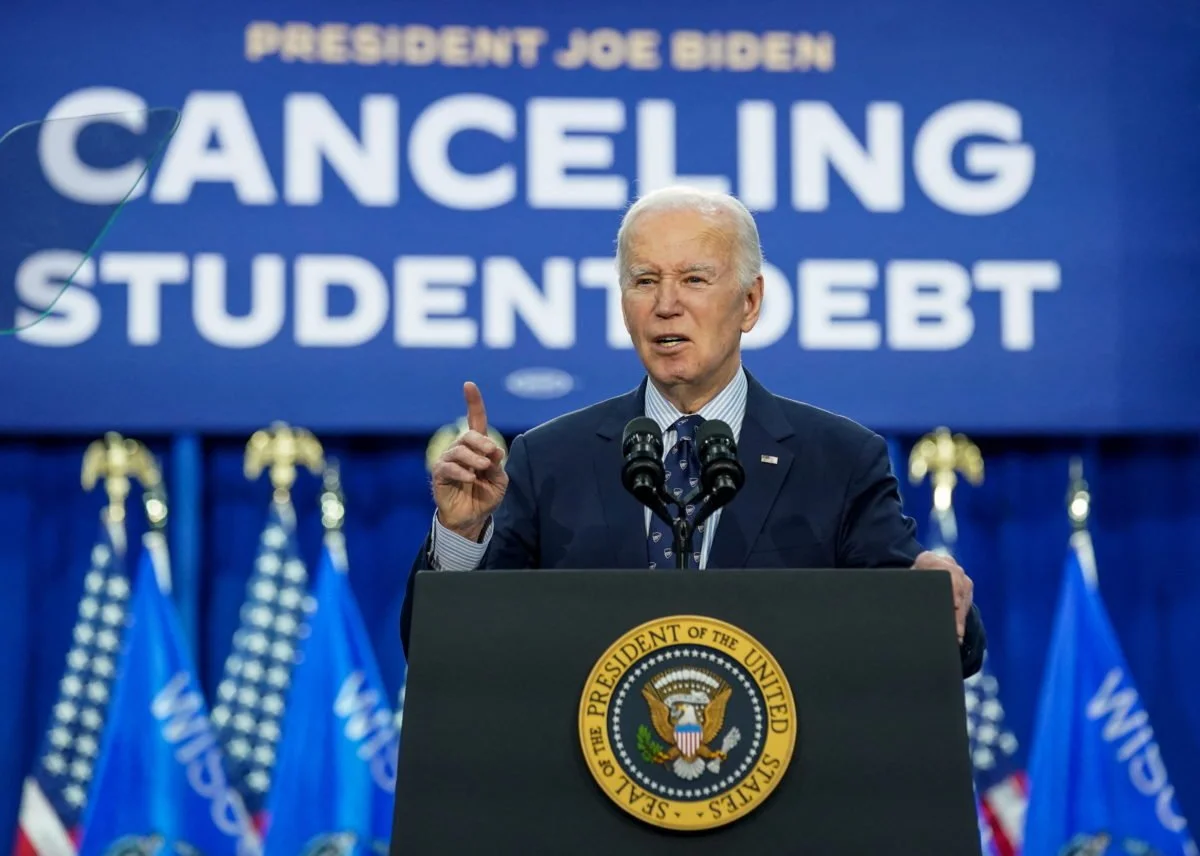

President Biden announcing his plan for federal student loan relief in Wisconsin after the Supreme Court struck down his use of the HEROES Act (April 8, 2024) | Credit: Kevin Lamarque/Reuters

Background

In 1958, Congress enacted the National Defense Education Act (NDEA) to ensure that Americans could keep up with increasing international competition. The NDEA authorized the first federal student loans, allowing each borrower a total of up to $1,000 each year.

In response to the 9/11 terrorist attacks, Congress was worried that borrowers who were in the military would need additional assistance. To address the problem, Congress unanimously passed the Higher Education Relief Opportunities For Students (HEROES) Act of 2001. The HEROES Act of 2001 vested the Secretary of Education with “specific waiver authority to respond to conditions in the national emergency” caused by the 9/11 attacks. When the HEROES Act of 2001 was set to expire in September of 2003, Congress passed the HEROES Act of 2003 to extend the coverage of the 2001 Act to include any war or national emergency, not just the 9/11 attacks. Under the 2003, Act, the Secretary “may waive or modify any statutory or regulatory provision applicable to the student financial assistance programs under title IV of the [Higher Education Act of 1965] as the Secretary deems necessary in connection with a war or other military operation or national emergency.”

In March of 2020, President Donald Trump signed the Coronavirus Aid, Relief, and Economic Security Act (CARES) Act into law to respond to the incoming COVID-19 Pandemic. The CARES Act set interest rates for student loans at 0% and suspended all payment requirements. The student loan pause under CARES Act was initially meant to only last six months, but it was extended by Trump in August and December 2020. During the 2020 presidential campaign, then-candidate Joe Biden pledged to cancel up to $10,000 of student loans for each borrower. On his first day of office, Biden signed the first of his seven extensions of the student loan pause.

On August 24, 2022, Biden announced his plan to use the HEROES Act to direct Secretary of Education Miguel Cardona to address the issue of student loans. Under Biden’s plan, borrowers with an adjusted gross income below $125,000 in either 2020 or 2021 would receive up to $10,000 of their loans forgiven. Pell Grant recipients, could receive up to $20,000. The Congressional Budget Office estimated that the plan would forgive approximately $430 million in total.

On September 29, 2022, Nebraska, Missouri, Arkansas, Iowa, Kansas, and South Carolina filed suit to challenge Biden’s program in the U.S. District Court for the Eastern District of Missouri. The district judge dismissed the case, finding that the states lacked standing to sue. The states appealed, and the U.S. Court of Appeals for the Eighth Circuit granted an injunction pending appeal.

In a separate case filed on October 10, 2022, two student loan borrowers who didn’t qualify for Biden’s plan challenged it in the U.S. District Court for the Northern District of Texas. In this case, the district judge issued an order to strike down the student loan forgiveness program. The Department of Education appealed, but the U.S. Court of Appeals for the Fifth Circuit declined to issue a hold on the order.

On December 12, 2022, the Supreme Court agreed to hear arguments for both cases together under the condensed title Biden v. Nebraska.

6 - 3 decision for Nebraska

Biden

Nebraska

Kagan

Roberts

Gorsuch

Thomas

Jackson

Barrett

Sotomayor

Alito

Kavanaugh

-

Writing for the Court, Chief Justice John Roberts began by explaining that the permission to “modify” under the HEROES Act doesn’t authorize “basic and fundamental changes in the scheme” that was designed by Congress. Instead, he stated that “modify” is “ordinarily used” as “’a connotation of increment or limitation,’ and must be read to mean ‘to change moderately or in minor fashion.’” Roberts found that the authority to “modify” only allows the Secretary to make “modest adjustments and additions to existing provisions, not transform them.”

Regarding the Secretary’s invocation of the waiver power over billions in student loans, Roberts found that it “does not remotely resemble how it has been used on prior occasions.” Roberts noted that previous Secretaries identified a specific legal requirement and waived it, while Secretary Cardona failed identify any provision of the Education Act that is being waived. Roberts further found that the Secretary’s “expansive conception” of the term “waive or modify” can’t “authorize the kind of exhaustive rewriting of the statute that has taken place here.”

Roberts noted that never before have powers of the magnitude of those being claimed here been previously claimed under the HEROES Act. In the past, waivers and modifications were “extremely modest and narrow in scope.” Roberts argued that under the broad reading of the HEROES Act argued for by the government, “the Secretary would enjoy virtually unlimited power to rewrite the Education Act ... the Secretary may unilaterally define every aspect of federal student financial aid, provided he determines that recipients have ‘suffered direct economic hardship as a direct result of a national emergency.’”

Roberts argued that this was a case of “the Executive seizing the power of the Legislature.” He noted that the Secretary’s claimed authority “’conveniently enabled [him] to enact a program’ that Congress has chosen not to enact itself.” Roberts pointed to the “sharp debates” ignited by the student loan forgiveness program to highlight that it stands “in stark contrast to the unanimity with which Congress passed the HEROES Act.”

Ultimately, Roberts concluded that the HEROES Act provides no authorization for the proposed student loan forgiveness plan when examined by using ordinary tools of statutory interpretation or searching for clear congressional authorization.

-

In her concurring opinion, Justice Amy Coney Barrett stated that she agreed with the majority’s holding, but wrote separately to address the major questions doctrine. She noted that ordinary tools of statutory interpretation were all that was needed for the Court to reach its conclusion, but that the major questions doctrine reinforces it.

Barrett began by acknowledging that the major questions doctrine may seem inconsistent with textualism if it’s viewed as a “substantive canon, or a rule that overrules the most natural reading of a text to internalize a specific policy value. However, she argued that the doctrine is actually an interpretive tool used to determine the text’s most natural meaning by emphasizing the importance of context.

Barrett argued that the major question doctrine reflects common sense regarding how Congress delegates authority, and used two analogies to explain why a broad, open-ended instruction should not always be read to its literal limit. In the first example, she explained that if a grocer tells a clerk to “go to the orchard and buy apples,” the clerk understands based on context from their past dealings and the size of the store that they shouldn't buy 1,000 apples if the store usually only stocks 200. In the second, she explained that if a parent tells a babysitter to “make sure the kids have fun” and hands over a credit card, it’s unreasonable for the babysitter to take the children on an overnight trip to an out-of-town amusement park. A reasonable person understands that a general instruction for “fun” covers local trips like ice cream or a movie, not massive excursions.

Barrett then connected these analogies to the relationship between Congress and executive agencies. Barrett explained that just as a parent would be expected to speak clearly if they intended to authorize a major trip, a “reasonably informed interpreter” expects Congress to speak clearly if it intends to assign decisions of vast “economic and political significance” to an agency. She argued that Congress normally intends to make major policy decisions itself and leaves only small details for agencies to handle during daily administration. Furthermore, because Article I vests “all legislative Powers” in Congress, it’s contextually more likely that Congress would make “big-time policy calls” itself rather than “pawning them off to another branch.”

Barrett concluded that the student loan forgiveness plan went far “beyond what Congress could reasonably be understood to have granted” in the HEROES Act. By applying the major questions doctrine as a tool of contextual interpretation, Barrett argued that the Court isn’t acting as a “policy arbiter,” but rather giving Congress’ words their best and most natural reading within a system of separated powers.

-

In her dissenting opinion, Justice Elena Kagan began by examining the plain text of the HEROES Act and argued that the Secretary of Education acted well within the broad authority granted by Congress to “waive or modify any statutory or regulatory provision” during a national emergency. Kagan criticized the majority for focusing almost exclusively on the word “modify,” which typically implies minor changes, arguing that it must be read alongside “waive,” which means to eliminate entirely. Kagan argued that if the Secretary has the power to eliminate a requirement (waive) or change it slightly (modify), then he surely has the power to do anything in between. Kagan stated that to suggest otherwise would make for an “insane” and “inconsequential” law that prevents the Secretary from responding to large-scale emergencies.

Kagan emphasized that the HEROES Act was specifically designed to handle national emergencies which are, by definition, major in scope and unpredictable. She pointed out that the goal of the HEROES Actw as to ensure that borrowers are not placed in a “worse position financially” because of a crisis, so by providing the Secretary with discretionary authority to apply new terms and conditions in lieu of old ones, Congress intended for the Executive to have the flexibility to offer meaningful relief, such as the student loan forgiveness plan.

Kagan strongly criticized the Court’s use of the major questions doctrine to strike down the plan, arguing that it has become a way for the Court to “negate broad delegations Congress has approved” simply because the Court finds the regulatory impact too significant. Kagan noted that Congress delegates broadly because agencies have expertise Congress lacks, and they can respond more quickly to changing circumstances. By requiring "heightened-specificity," the Court is making it nearly impossible for Congress to ensure adequate responses to unforeseen events.

Kagan concluded by warning that the majority’s decision was a threat to both the separation of powers and democratic order. She pointed out that the Secretary and the President are politically accountable to the voters for the success or failure of their policies, but the members of the Court are “detached from the body politic.” She stated that by refusing to respect the full scope of the delegation made by Congress, Court had transformed itself into the “arbiter—indeed, the maker—of national policy.”